On July 19, 2026, MetLife Stadium in New Jersey will host the finals of the first-ever tri-country FIFA men’s World Cup, hosted by Mexico, Canada, and the United States. That same month, trade policy watchers will be following a different matchup for this North American trio: the joint review of the US-Mexico-Canada Agreement (USMCA). The incoming Trump administration will need to take advantage of the USMCA’s renewal process to address strategic objectives, without putting the agreement itself at risk. Any downgrade in trade relations from new tariffs will have serious impacts on the North American economy—including on US exporters.

The USMCA is set to terminate in 2036 at the close of its sixteen-year term. When the trio meets in July 2026, they can renew the agreement for a second sixteen-year term. However, if any one of the three decide not to renew the agreement, the trio will meet every year until they either agree to renew the USMCA—or run out of time before it expires in 2036. Although cumbersome, this process is designed to provide an opportunity for the three countries to regularly adapt the terms as they see fit. No other trade agreement has such an adaptable structure, providing an unprecedented opportunity to optimize trade within North America.

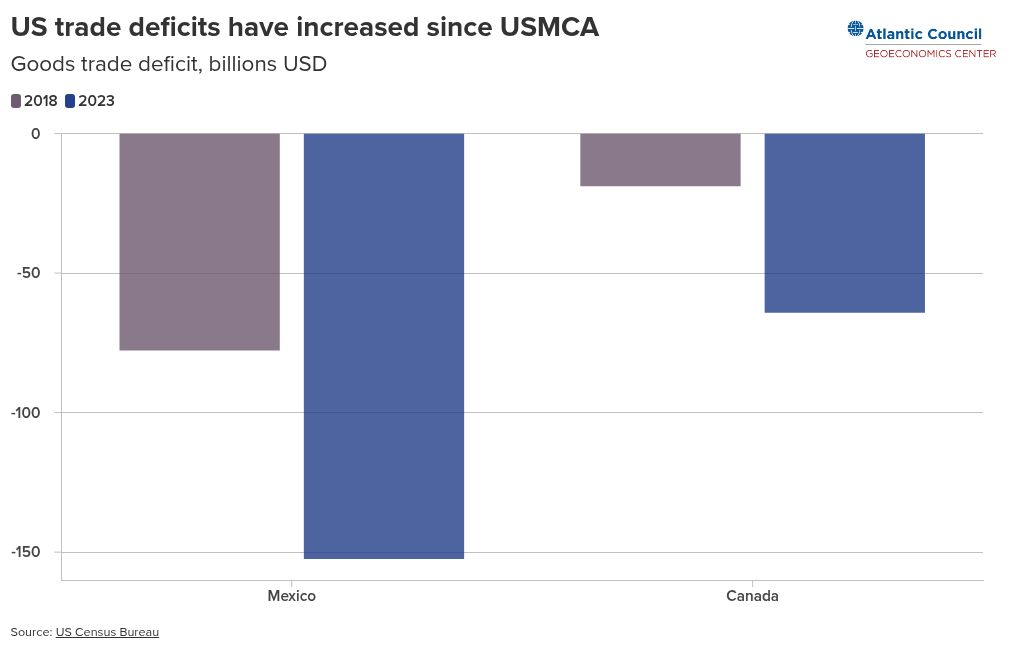

It’s possible that few other trade agreements will also have as much political pressure as the USMCA in 2026, with a range of issues now attached to its renewal including immigration, shipment of illegal drugs, and concerns about Chinese goods subject to tariffs making their way freely to the United States through the USMCA. The incoming administration’s fixation on the United States’ trade deficits with Mexico and Canada is perhaps the most traditional topic under review.

The Trump administration’s proposed approach to these concerns is to create uncertainty through higher tariffs in order to negotiate better terms in the agreement. If the Trump administration does increase any tariffs on USMCA partners, except due to national security concerns, it will violate the terms of the agreement under Article 2.4. Canada and Mexico would likely retaliate by levying import duties of their own, effectively removing the free trade advantages provided by the USMCA. This will prove expensive and destabilizing for any company dependent on the highly integrated North American supply chains. These are the very same exporters on whom the administration relies for support. Before the administration would need to take that approach, it’s important to understand the economic leverage—and dependencies—each country has with the others.

At the negotiating table

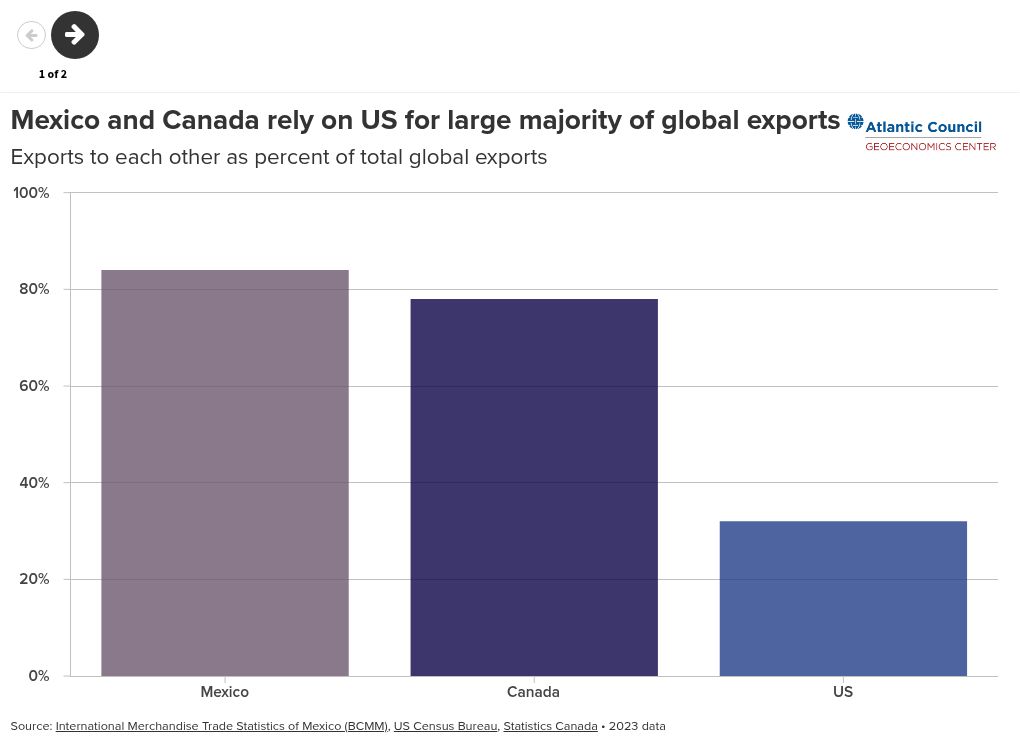

Canada and Mexico rely on the US economy far more than the United States relies on either of them—although the relationship is important for all three. Mexico and Canada sold 80 percent and 76 percent, respectively, of their exports to the United States in 2023. Comparatively, 32 percent of US exports in 2023 went to Canada and Mexico combined.

The asymmetry here engenders a higher level of political importance for the USMCA within Mexico and Canada. Employment in Mexico is especially dependent on trade with the United States. When negotiations begin in 2025, Mexican President Claudia Sheinbaum will be under an entirely different level of pressure from her citizens to maintain favorable trade relations with the United States and Canada. The cards are favorably stacked for the United States to have the heaviest hand in negotiations––even without the threat of higher tariffs.

In support of US jobs

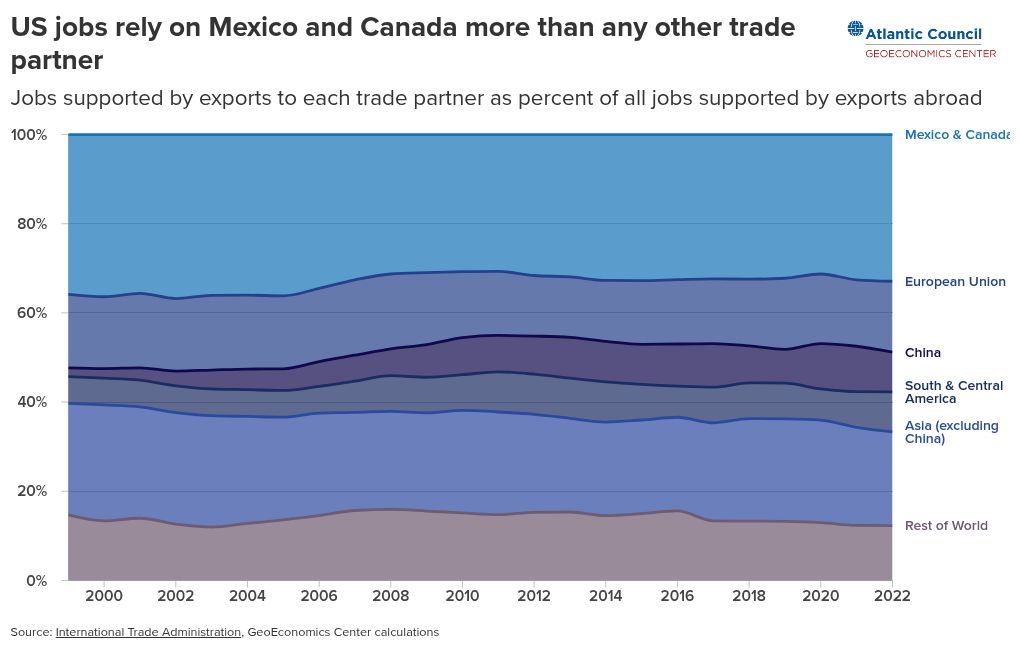

Even so, the United States has deep political interests in maintaining the USMCA. From Washington’s side, the agreement’s guiding objectives—creating more balanced trade in support of high-paying jobs in the United States—has been a point of continuity for businesses, receiving bipartisan support throughout the last four years. Of all the jobs in the United States that are supported by exports abroad, 33 percent are supported by exports to Mexico and Canada. No other regional trade relationship has a larger impact on US exporter jobs.

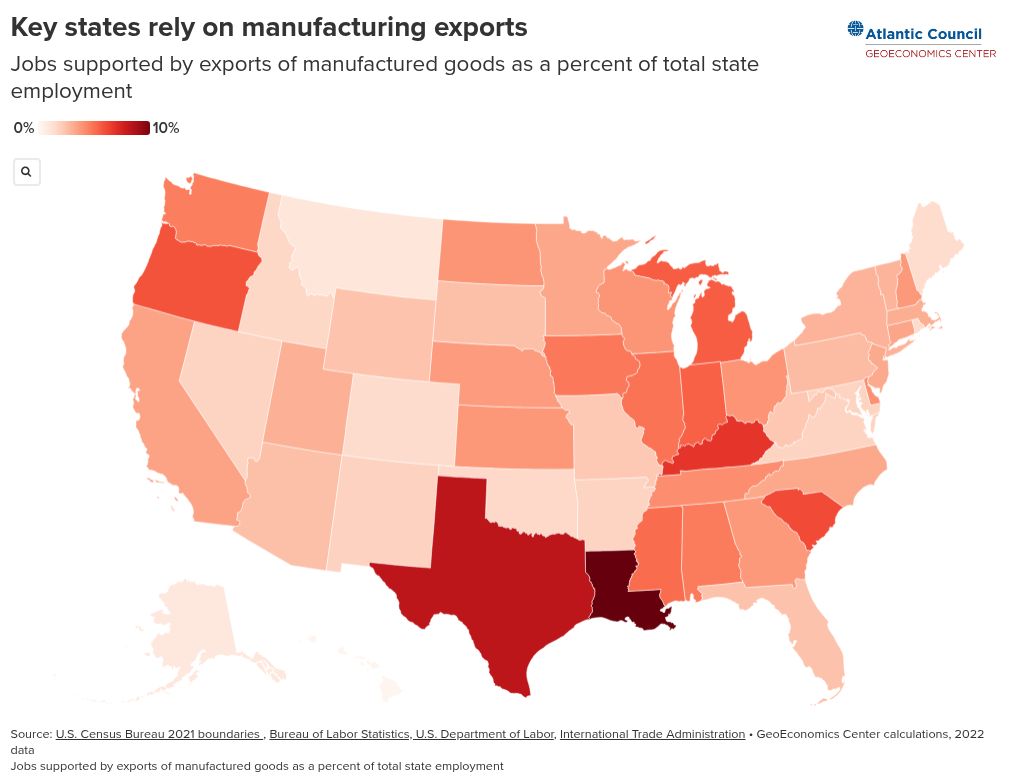

Although jobs supported by the USMCA make up only roughly 2 percent of total jobs in the United States, the agreement has outsized importance within key Republican constituencies. The incoming Trump administration, with its promise of creating a “manufacturing renaissance” with “millions of jobs” will need to consider that exports support roughly 40 percent of manufacturing jobs in the United States.

As for the USMCA, roughly a quarter of the US jobs supported by exports to Canada and Mexico are in manufacturing, with automobile manufacturing employing the most individuals. Manufacturing export jobs have a relatively greater importance on employment in red states—as well as key swing states such as Michigan and Wisconsin. These linchpin states helped the incoming president win the 2024 election; trade disruptions here could have high domestic political costs for the administration.

If the United States increases import tariffs and Canada and Mexico apply retaliatory tariffs, US exports will be more expensive and less profitable. Oxford Economics estimates that the proposed 25 percent tariffs would decrease trade in North America by 50 to 60 percent, which would push Canada into a recession in 2025. US exports to Canada, and, by extension, export-supported jobs would likewise falter due to slow demand. If the incoming Trump administration wishes to improve the odds for US exporters, it should maintain favorable trade conditions with the top buyers of US goods: Canada and Mexico.

Manufacturers are also importers

Of course, Mexico and Canada are not only buyers of US goods, but are also suppliers of US inputs. Tariffs will increase the cost of importing these goods, which will weigh on manufacturers’ overall production costs. Historically, higher input costs have been shown to have a negative impact on manufacturing employment. The increased input costs from the March 2018 steel tariffs directly lead to the loss of approximately 75,000 manufacturing jobs by the middle of 2019.

Furthermore, trade within North America is highly integrated to the point that it might best be described as “circular.” Supply chains are so connected in part because of the incentive structure provided by the USMCA and its predecessor, the North American Free Trade Agreement. To qualify for duty-free trade, goods must meet rules-of-origin requirements, which generally require at least 60 percent of the value of a good to be made with regional inputs, or “content.” This influences companies to develop supply chains that cross North American borders multiple times throughout the production process—locating each phase of production where they can optimize costs. As a result, for each dollar that the United States imports from Mexico in manufactured goods, close to 30 cents is likely made up of US content, according to assessments based on the structure of these supply chains. The United States’ trade deficits with Mexico and Canada, therefore, might be viewed as much less problematic than deficits with other partners because the imports from these countries help generate demand for exports to these partners and are made up of US goods.

Assuming Mexico and Canada would retaliate in the event of US tariffs, each time a good moved across borders throughout the production process, the importer would have to pay a tariff, raising costs at every stage of the production process. A US company operating in Mexico, for example, might then be incentivized to relocate fully to the United States to avoid the tariff. On the other hand, the cost differential in doing so could be so great for some products that it might be more profitable to continue producing outside of the United States—even with the tariffs in place. In this case, consumers would still pay higher prices while supply chains stay intact.

With any increased barriers to trade among the United States, Mexico, and Canada, the administration should expect businesses to face added costs and risks from secondary effects. This includes the added costs companies would face purely from navigating the new legislative changes and in adjusting supply chains accordingly. For example, companies would likely attempt to receive exemptions from tariffs while adjusting production plans in the interim, which has labor costs and may cause production delays. These costs will weigh on small- and medium-size companies the most, as they have fewer resources to dedicate to managing their global supply chains.

Igniting a manufacturing “renaissance”

If the incoming administration wants to accomplish its goal of a US “manufacturing renaissance,” it should consider updating how the USMCA incentivizes manufacturing and fairer wages within the continent.

One such incentive is the regional content requirement. To improve the agreement in a way that generates political support, the United States should better enforce these requirements by evaluating nonregional (i.e. Chinese) companies that operate in North America to better determine if the content is truly local. The United States, Mexico, and Canada should consider if a 100 percent Chinese-owned business should be able to reap the benefits of the USMCA. It also matters how this legislation is written; the 2026 negotiations should prioritize closing any loopholes in its description of regional content.

Automotive manufacturing has the most advanced incentive structure under the USMCA and might be used as a model for a wider range of commodities. Under the USMCA, each vehicle must be produced with 75 percent regional content to satisfy the rules-of-origin requirements. Furthermore, 40 to 45 percent of the value-added content in any auto import must be made by workers making at least sixteen dollars an hour. This reduces offshoring incentives by making production in the United States more competitive, allaying a key fear.

To meet its objective of supporting US jobs, the White House could advocate for higher value-added content requirements or add a minimum wage requirement for critical manufactured products beyond automotive goods. To minimize disruptions to businesses and supply chains, the administration could propose a phased approach, whereby regional content and wage requirements would increase gradually throughout the next decade. This would still have to be targeted, of course, in order to make supply chains cost-effective, but would be a more business-friendly way to change the incentive structures to favor US and North American manufacturing.

The incoming administration has a strong enough advantage for the coming negotiations that it can expect to improve the agreement––and ensure the USMCA remains in place long after Trump leaves office.

Sophia Busch is an assistant director at the Atlantic Council’s GeoEconomics Center.

Further reading

Image: US President Donald Trump checks a pen during a signs the United States-Mexico-Canada Trade Agreement (USMCA) during a ceremony on the South Lawn of the White House in Washington, U.S., January 29, 2020. REUTERS/Jonathan Ernst

This post was originally published on here